After a heavy storm rolls through South Jersey, the first question on most homeowners’ minds is whether their insurance will pay for whatever happened to the roof. It’s a fair worry — and the honest answer is more nuanced than a simple yes or no.

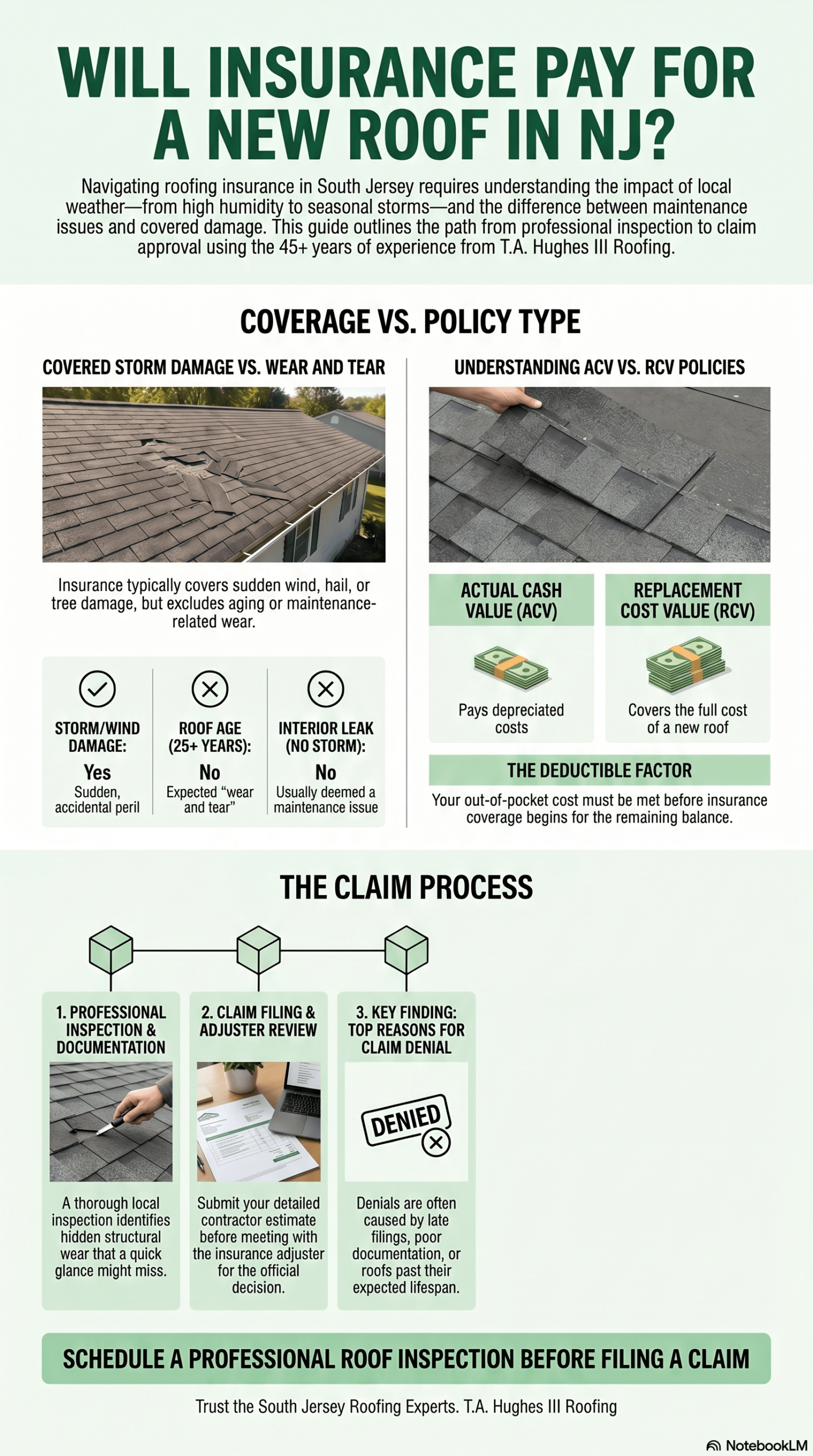

In some cases, New Jersey homeowners insurance may pay for a new roof — but only when the damage is sudden and caused by a covered event, such as a windstorm, hail, or a fallen tree. Insurance is generally not designed to pay for a roof that has failed due to age, normal wear, or lack of maintenance. The actual answer depends on your specific policy, your roof’s condition before the damage occurred, and the cause of the damage itself.

Will Insurance Pay for a New Roof in New Jersey?

Homeowners insurance may help pay for roof repair or replacement in New Jersey when the damage is caused by a covered event such as wind, hail, falling debris, or sudden storm damage. Insurance usually does not cover normal aging, wear and tear, poor maintenance, or long-term roof deterioration. A professional roof inspection can help document visible damage before you speak with your insurance company.

Key Takeaways

- Homeowners insurance in New Jersey is built to cover sudden, accidental damage — not gradual wear, aging, or deferred maintenance.

- Wind, hail, and falling trees are among the most common covered causes of roof damage in South Jersey.

- Policy type matters: Replacement Cost Value (RCV) policies pay closer to actual replacement cost, while Actual Cash Value (ACV) policies factor in depreciation.

- Your deductible always applies, and older roofs may face reduced coverage, separate wind/hail deductibles, or full exclusions.

- The insurance company makes all coverage decisions — not the contractor. Honest documentation and a thorough inspection give you the clearest picture of your options.

What Does Homeowners Insurance Actually Cover for Roofs?

Most standard homeowners policies in New Jersey are written to cover sudden and accidental damage from specific causes, often called “covered perils.” For roofing, these typically include:

- Wind damage

- Hail damage

- Damage from falling objects (such as tree limbs)

- Damage from the weight of ice or snow

- Fire and lightning damage

Insurance policies are not maintenance plans. They’re designed to respond to unexpected events — not the normal aging process every roof goes through.

In South Jersey, the majority of roof-related claims tend to follow major weather events — especially the high winds and heavy rain that come with summer thunderstorms and Nor’easters. From Mount Laurel to Cherry Hill to Mullica Hill, the damage patterns we see after a serious storm tend to look similar: lifted shingles, wind-creased shingles, flashing problems, and the occasional fallen limb.

What Types of Roof Damage Are Usually Covered?

Damage that happens during a single, identifiable event is generally what insurance is built to address. In our experience working on homes throughout Burlington, Camden, and Gloucester Counties, this usually includes:

- Wind-lifted or missing shingles following a storm with documented high winds

- Impact damage from fallen tree limbs or branches

- Hail damage that creates impact marks on shingles, flashing, or vents

- Sudden water intrusion caused directly by storm-related damage

- Compromised flashing or roofing components following a covered event

Coverage almost always comes down to three things: the cause of the damage, the date it occurred, and the condition of the roof beforehand.

What Types of Roof Damage Are Usually Not Covered?

This is the part that surprises many homeowners. Standard policies typically do not cover:

- Granule loss from age

- Curling, cupping, or worn shingles from normal weathering

- Leaks caused by deferred maintenance

- Flashing failures from age or worn-out sealants

- Pre-existing damage that wasn’t reported or repaired

- Damage that develops gradually over months or years

Many South Jersey homes — especially those built between the 1970s and 1990s in towns like Marlton, Voorhees, and Washington Township — are now reaching the end of their first or second roof’s expected lifespan. When these roofs begin to fail, it’s almost always due to age. That’s not what insurance is built to address.

How Does ACV vs. RCV Affect What You Receive?

Two important policy terms shape what an insurance payment actually looks like:

Actual Cash Value (ACV): The insurance company pays the depreciated value of the roof, meaning age and wear are subtracted from the payment. On an older roof, this number can be significantly lower than the cost of a new one.

Replacement Cost Value (RCV): The insurance company pays based on what it would cost to replace the damaged roof with one of similar quality. Depreciation may be held back initially and released after the work is completed.

Many newer policies in New Jersey also include separate wind and hail deductibles, sometimes calculated as a percentage of the home’s insured value rather than a flat dollar amount. Reading the policy carefully — or speaking directly with your agent — is the only reliable way to confirm which type of coverage you have.

Common Misconceptions About Roof Insurance Claims

Over the years, a few homeowner assumptions come up again and again. Worth clearing up gently:

- “All storm damage is automatically covered.” Coverage depends on the policy, the deductible, and the condition of the roof before the storm.

- “If insurance pays, I get a brand-new roof at no cost.” The deductible always applies, and ACV policies pay less than the full replacement cost.

- “A contractor can guarantee my claim will be approved.” No contractor can promise that. Coverage decisions belong to the insurance company alone.

- “If I wait, the damage will be more obvious and easier to claim.” The opposite is usually true — delays make it harder to tie damage to a specific storm event.

- “My old roof is covered the same as a newer one would be.” Many policies treat older roofs differently, with reduced coverage, ACV-only payouts, or age-related exclusions.

What Does the Typical Insurance Claim Process Look Like?

Every insurer handles claims a little differently, but the general path usually looks like this:

- Damage occurs, typically during or after a storm or sudden event.

- The homeowner documents the damage with photos and notes the date.

- A roof inspection is performed to evaluate what’s there and identify the cause.

- A claim is filed with the insurance company.

- An insurance adjuster inspects the roof and writes their scope of damage.

- The contractor reviews the adjuster’s findings and provides a written estimate.

- The insurance company issues a coverage decision and any payment based on the policy terms.

- Repair or replacement work is completed.

The contractor’s role is to document conditions accurately and explain findings clearly. All coverage decisions belong to the insurance company.

Why Do Some Claims Get Denied or Only Partially Paid?

Common reasons we see in South Jersey include:

- The damage was determined to be from age or wear, not a covered event

- The roof was already at the end of its lifespan before the storm

- Pre-existing damage wasn’t disclosed to the insurer

- The claim wasn’t filed within the policy’s time limits

- Documentation was incomplete or unclear about the date of damage

- The deductible was higher than the cost of repairs

A denial doesn’t always mean the homeowner did something wrong. Often, it simply means the policy didn’t cover the specific type of damage that occurred.

What Should Homeowners Do Before Filing a Claim?

Before contacting the insurance company, it usually helps to:

- Get a professional roof inspection so you understand what’s actually damaged

- Document the damage with clear photos and note the date it was first noticed

- Review your policy so you know your deductible and coverage type

- Save records of any prior maintenance or repairs

A clear, accurate picture of the roof’s condition makes the claim process much smoother — whether the outcome is a covered claim, a denial, or something in between.

FAQ

Will my insurance company drop me if I file a roof claim? Filing a single claim doesn’t automatically lead to non-renewal, but multiple claims over a short period can affect a policy. Your insurance agent is the best person to answer this for your specific situation.

Does my roof’s age affect my coverage? Yes. Many insurers reduce coverage, switch to ACV-only, or place limits on roofs over a certain age — often 15 to 20 years. Some policies now require an inspection before renewing coverage on older roofs.

Can I file an insurance claim for a roof leak? You can file, but coverage depends on the cause of the leak. Sudden storm damage that causes a leak may be covered. Leaks from age, wear, or maintenance issues generally are not.

How long do I have to file a roof damage claim in New Jersey? Most policies require prompt reporting after the damage occurs, often within a specific window. Check your policy language or ask your insurance agent for the exact time limits that apply to you.

Do I need multiple estimates for my insurance claim? Most New Jersey insurers don’t require multiple estimates, though they typically expect a written scope of work from a licensed contractor. The insurance adjuster will also write their own estimate as part of the process.

What happens if my claim is denied? A denial isn’t always the final word — many insurers have a reconsideration process, and clearer documentation can sometimes change the outcome. Your insurance company is the right place to start that conversation.

Not Sure if Your Roof Damage Qualifies?

If a recent storm has you wondering whether your roof took damage — or whether what you’re seeing is from age or weather — a thorough inspection is the clearest way to find out. We’ll walk the roof, document what we find, and explain it to you in plain language. No pressure, no sales push, just an honest look at what’s there so you can make an informed decision.

[Schedule a free roof inspection →]

Related Reading

- What a Professional Roof Inspection Should Actually Cover

- How Water Actually Moves Through a Roof and Into a Home

- What Parts of a Roof Tend to Fail First

- What Roof Flashing Is and Why It Fails

- Why Small Roof Leaks Turn Into Bigger Problems Over Time

T.A. Hughes III Roofing has been serving Burlington, Camden, and Gloucester Counties for over 45 years. We’re a family-owned exterior remodeling contractor specializing in honest evaluations, clear written estimates, and craftsmanship built for South Jersey’s climate.